Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

L1 Value Capture Shrinks Significantly, ETH, SOL, HYPE Struggle to Return to All-Time High

Original Title: The Compression of L1 Value Capture

Original Source: Pine Analytics

Original Translation: Ethan, Odaily Planet Daily

Editor's Note: In the past few years, the crypto market has once believed that the transaction fee revenue of Layer 1 blockchains is the core cash flow supporting token valuation. However, this study used on-chain data to uncover a different fact: whether it's Bitcoin's congestion cycles, Ethereum's DeFi and NFT peaks, or Solana's memecoin frenzy, all transaction fee booms will eventually be compressed by innovation. Demand surges bring income peaks, and these peaks stimulate alternative solutions to emerge, causing profits to be systematically squeezed out. The compression of L1 value capture is not a cyclical phenomenon but a structural outcome of open networks.

By 2026, the market no longer simply values L1 based on "fee capture." The price driving forces of ETH and SOL are shifting from L1 fee logic to staking rewards, ETF capital flows, RWA narratives, protocol upgrade expectations, and the macro liquidity environment. The compression trend continues, but the pricing anchor has already shifted. What is truly worth considering is not just whether transaction fees will continue to decline but rather: when the market no longer prices L1 based on "on-chain profits" but instead uses "asset narratives" and "structural capital flows" for pricing, whether this new logic is equally fragile; and when the narrative fades, what kind of fundamental support the price will return to.

L1 blockchains, in their stage of scaling development, find it challenging to continuously and stably earn transaction fees. Every major income source they once identified—from transaction fees to MEV—will eventually be eroded bit by bit by the users they serve through various arbitrage methods. This is not because a particular chain did not perform well but rather due to the inherent nature of open, permissionless networks: as soon as the money L1 earns from fees reaches a certain scale, transaction stakeholders will find new ways to compress this income or even reduce it to zero.

Bitcoin, Ethereum, and Solana are considered some of the most successful networks in the crypto space. Interestingly, despite processing billions of dollars in value flow every day, these three have followed almost the same path: transaction fee revenue suddenly surges in the short term, attracting everyone's attention, but before long, it is seized by L2 (layer 2 networks), private order flows, MEV-aware routing tools, or new gameplay at the application layer. This situation has repeatedly occurred in every transaction fee model in the crypto industry, every MEV fluctuation cycle, and every scaling solution, with no signs of slowing down.

This article argues that L1 transaction fees being compressed is a long-standing and accelerating trend. This article will outline the specific innovative plays that can compress profits at different stages, and also explore what this means for L1 tokens that still factor "earning sustainable revenue through transaction fees" into their valuation.

Bitcoin

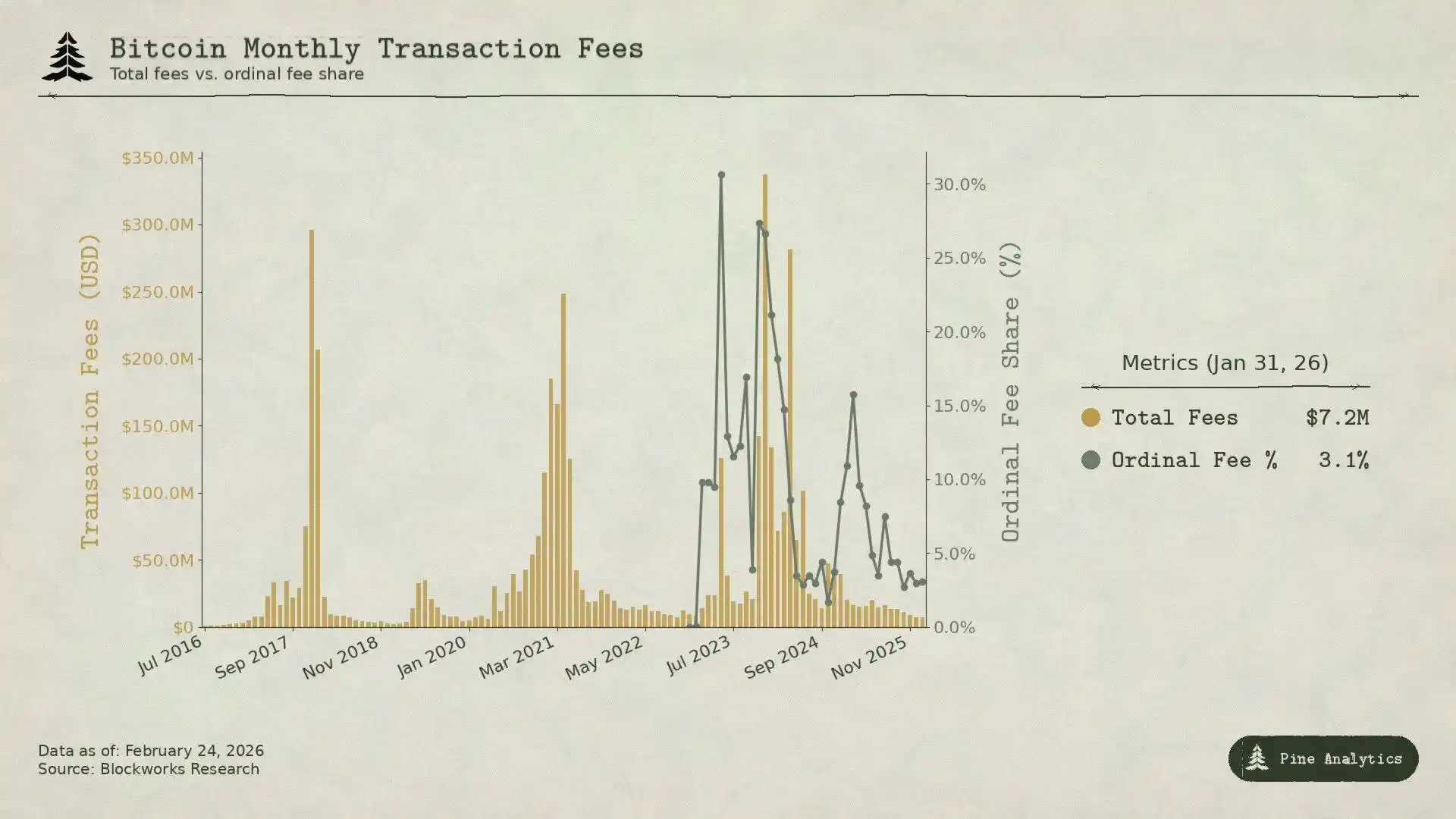

Bitcoin's transaction fees heavily rely on on-chain congestion during BTC transfers to earn fees—everyone rushes to make transfers, naturally driving up fees. Additionally, because Bitcoin doesn't have smart contracts, there is almost no such thing as MEV on the network. The key issue is this: whenever BTC price surges and transaction fees spike, the fee increase relative to the economic activity at that time is much weaker compared to the previous cycle.

Back in 2017, when BTC surged from $4,000 to $20,000, the average fee skyrocketed from less than $0.40 to over $50. At the peak on December 22, fees accounted for 78% of the miner block reward: fees alone were around 7,268 BTC, nearly four times the block subsidy. Yet, in just three months, fees plummeted by 97%, reverting to their original state.

The market responded exceptionally fast and solutions emerged quickly. In early 2018, SegWit transactions only accounted for 9%, growing to 36% by mid-year; though these transactions represented over a third of the total volume, they contributed only 16% of the fees. Exchanges also started batch processing, consolidating hundreds of withdrawals into a single transaction, saving a significant amount of fees. With these factors combined, fees dropped by 98% in six months. Additionally, the Lightning Network officially launched in early 2018 to address the fee issue with small transactions, and other on-chain Wrapped BTC solutions allowed users to hold BTC exposure without needing to operate on the Bitcoin main chain.

By the peak of BTC's price in 2021, despite the price reaching $64,000, monthly fee income was even lower than in 2017. At that time, there were fewer on-chain transactions, but the dollar-denominated transfer volume was 2.6 times higher than in 2017—simply put, there were more network transfers, but the fees that could be earned did not keep up, and even decreased.

In the current cycle, this trend is even more evident. With BTC rising from $25,000 to over $100,000, an increase of roughly 3x (the original text says 4x, adjusted slightly to reflect the actual price range without changing the original intent), standard transfer fees have never experienced the same explosive growth as in previous cycles. By the end of 2025, daily transaction fees will be approximately $300,000, which is less than 1% of total miner revenue. In 2024, Bitcoin's annual transaction fees amounted to $922 million, but most of it came from the short-term hype around Ordinals and Runes, not stable revenue from traditional BTC transfers. By mid-2025, mainstream Bitcoin ETFs already hold over 1.29 million BTC, about 6% of the total supply, providing the market with considerable BTC exposure demand, yet generating no on-chain transaction fees. The on-chain interactions needed to acquire Bitcoin assets have been largely engineered out.

Ordinals and Runes once in April 2024 pushed the fee-to-miner ratio to 50% of the block reward, but as related tools matured, by mid-2025, this ratio had dropped back to below 1%. This short-term spike was more reminiscent of MEV windfalls rather than stable income from congestion, driven by immature tooling around new assets rather than genuine demand for BTC settlement.

This pattern is actually quite clear: whenever Bitcoin makes enough visible money from fees, cheaper alternatives emerge in the ecosystem. L1 can only earn one short-term fee peak from each use case, with subsequent profit continuously eroded by innovation.

Ethereum

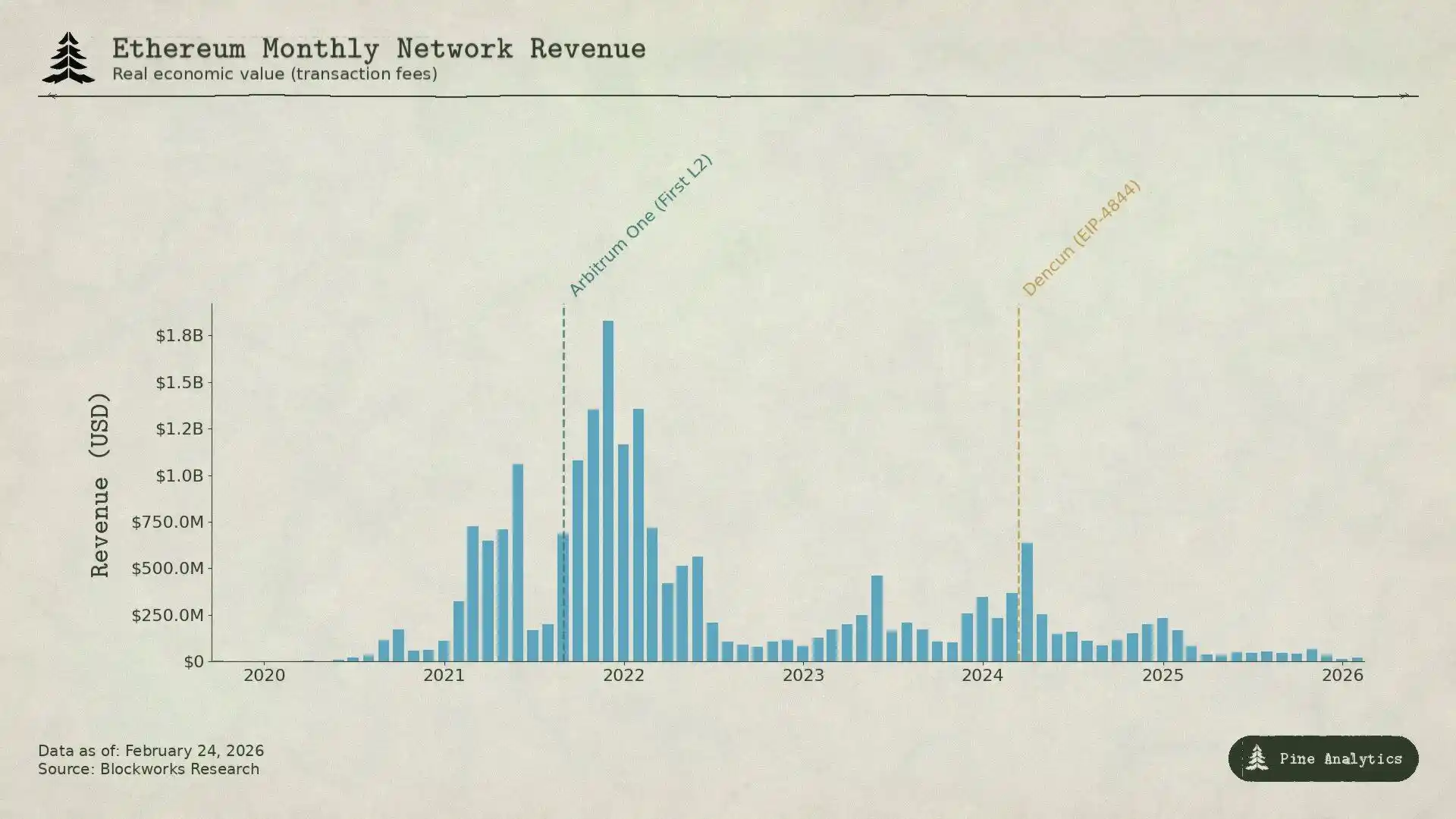

Ethereum's fee story is even more dramatic. This chain truly captured massive value, only to witness it being systematically dismantled.

In mid-2020, 'DeFi Summer' positioned Ethereum as the epicenter of the new financial system. Uniswap's monthly volume surged from $169 million in April to $15 billion in September. TVL grew from under $1 billion to $150 billion by year-end. In September 2020, Ethereum miners hit a record $166 million in fee revenue, six times that of Bitcoin miners. This was also the first time a smart contract platform earned sustained and substantial income from real economic activity.

In 2021, NFTs layered on top of DeFi. Average transaction fees peaked at $53. Quarterly fee revenue increased from $231 million in Q4 2020 to $4.3 billion in Q4 2021, a growth of 1,777%. EIP-1559, implemented in August 2021, introduced a base fee burn mechanism, permanently removing some fees from circulation. At that time, Ethereum seemed to have truly addressed the core issue of L1 not making money.

However, these fees are essentially 'congestion fees': users pay $20 to $50 transaction fees not because the transaction itself is worth that much, but because everyone is trying to use the chain, exceeding Ethereum's processing capacity of roughly 15 transactions per second (15 TPS). This inherent limitation has also provided ample room for cheaper alternatives.

Other L1s like Solana, Avalanche, BNB Chain can provide transaction services for just a few cents; Ethereum's L2 Rollups, such as Arbitrum and Optimism, have captured a good amount of business—they process transactions on their own networks, then batch the compressed transactions back to the Ethereum mainnet for settlement, fast and cheap.

Subsequently, Ethereum underwent a "self-nerf." The Dencun upgrade on March 13, 2024, introduced Blob transactions (EIP-4844), providing a cheaper data publishing path for Layer 2. Prior to this, L2 used calldata, costing around $1,000 per megabyte. Post-upgrade, Arbitrum's single transaction fee dropped from $0.37 to $0.012, and Optimism's from $0.32 to $0.009. The median fee in Blob almost dropped to zero. Ethereum initially hoped to retain users with this but unexpectedly weakened its last significant fee revenue source.

Looking at the data makes it more intuitive. In 2024, L2 generated $277 million in revenue but only paid around $113 million to Ethereum. By 2025, L2 revenue had dropped to $129 million, with a flowback to Ethereum of only about $10 million, less than 10% of L2 revenue, a year-on-year drop of over 90%. The once over $100 million monthly L1 fee revenue had plummeted to below $15 million in the fourth quarter of 2025. This chain that generated $4.3 billion in revenue in a single quarter saw its revenue shrink by about 95% just four years later.

Bitcoin's revenue was compressed because people could get BTC off-chain; Ethereum's revenue was compressed in two waves:

The first wave was other alternative networks, which attracted users who did not want to spend high congestion fees;

The second wave was Ethereum's own scaling plan, which reduced the cost of L2 transmitting data to almost zero, and Ethereum itself could no longer make money through settlements. Regardless of which kind, L1 either built or allowed those tools that took away its revenue to appear.

Solana

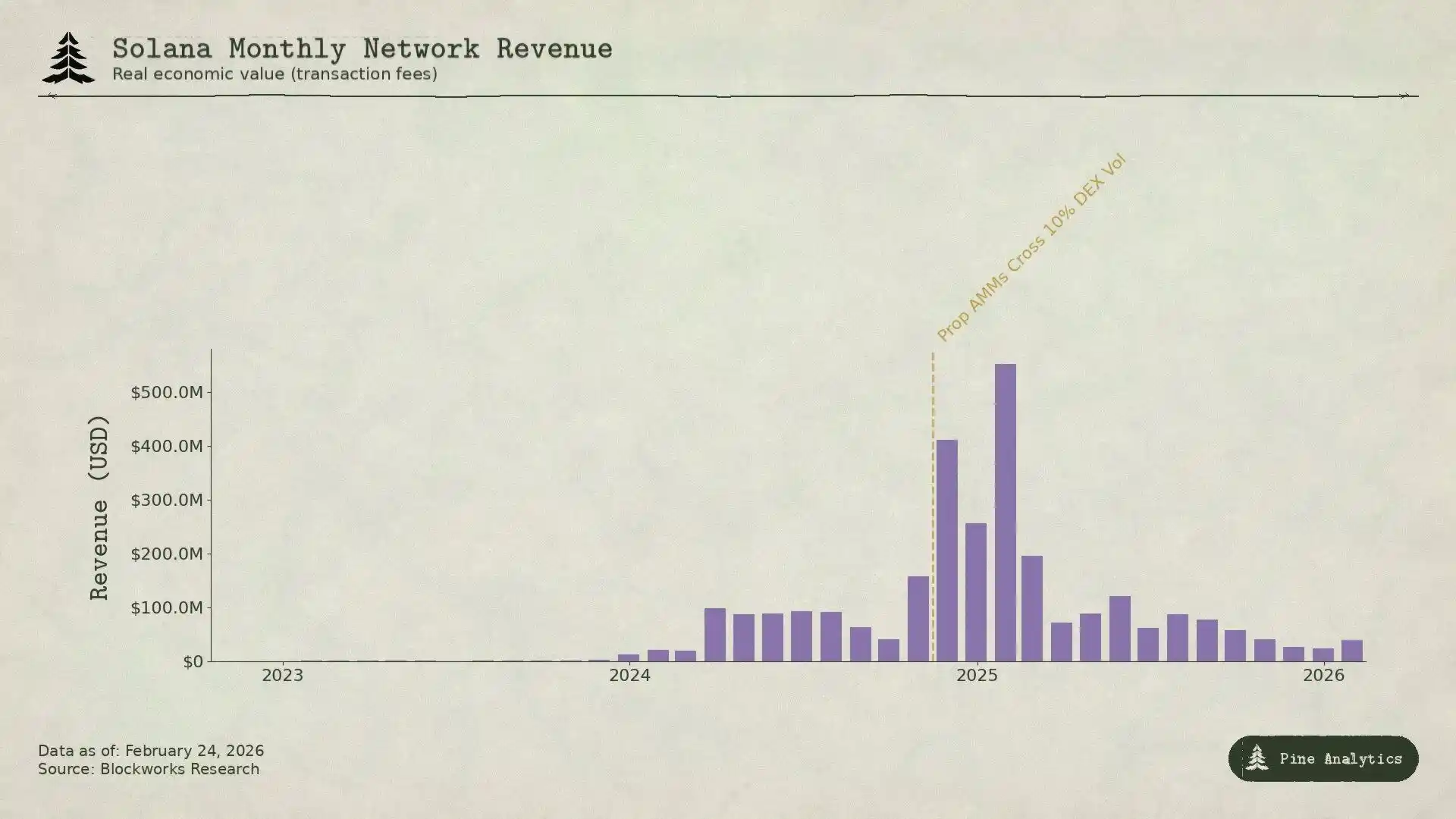

The logic behind Solana's revenue generation is completely different from Bitcoin and Ethereum—it hardly relies on congestion to earn fees. The base fee is fixed at 0.000005 SOL per signature, so cheap that it can almost be ignored. About 95% of the fee revenue comes from priority fees and MEV tips paid through the Jito block engine. In the first quarter of 2025, Solana's Real Economic Value (REV) reached $816 million, with 55% coming from MEV tips. In 2024, validators could earn around $1.2 billion, with operational costs of only about $70 million, leaving significant profit margins.

The key driver of the Solana fee explosion was memecoin trading. Pump.fun, launched in January 2024, generated over $6 billion in protocol revenue in less than 18 months, with memecoin issuance peaking at 99% during its heyday. DEX daily trading volumes once reached $380 billion. In January 2025, the TRUMP token launch sent single-day priority fees skyrocketing to 122,000 SOL, with MEV tip amounts hitting 98,120 SOL. In 2024, the top 1% of memecoin traders contributed $1.358 billion in fees, representing nearly 80% of total memecoin fees, mostly driven by MEV.

Today, two types of innovation are curtailing this revenue stream.

The first is proprietary AMMs. Protocols like HumidiFi, SolFi, Tessera, ZeroFi, GoonFi, among others, employ private treasuries managed by professional market makers, offering internal quotes updated multiple times per second. As liquidity is not publicly exposed, MEV bots cannot front-run trades. Crucially, proprietary AMMs route orders through aggregators like Jupiter, actively selecting counterparties instead of passively exposing themselves to any participant willing to pay an MEV bribe. By keeping pricing private and consistently refreshed, they eliminate the issue of "stale quotes," a major source of Solana's considerable MEV income. HumidiFi processed nearly $1 trillion in transaction volume in its first five months post-launch. Today, proprietary AMMs represent over 50% of Solana DEX trading volume, even higher in high-liquidity pairs like SOL/USDC.

The second is Hyperliquid, which directly migrates the most profitable spot trading activity off Solana. Leveraging its in-house HyperCore technology, it developed a native bridging solution allowing tokens on Solana to be deposited into and withdrawn from Hyperliquid and traded on its spot order book. When Pump.fun introduced the PUMP token in July 2025, price discovery occurred on Hyperliquid, not Solana's DEX, facilitated by the HyperCore cross-chain bridge. Prior to this, Hyperliquid had already trialed this model with SOL itself and tokens like FARTCOIN—during the phase of maximum price impact, volatility, and MEV profitability at the token's initial pricing, they had already started moving off Solana.

These two play-to-earn mechanisms squeeze Solana's revenue from both directions: The proprietary AMM reduces MEV transactions left on Solana, while Hyperliquid moves the most MEV-profitable spot trades off-chain. By the second quarter of 2025, Solana's REV decreased by 54% compared to the previous quarter, leaving only $272 million; daily MEV tip fees dropped by over 90% from the January peak, now less than 10,000 SOL per day.

In fact, the pattern is the same as the first two chains, just the way of making money is different:

Solana's fees are essentially short-term money earned through MEV when the new transaction gameplay first emerged, and things were still relatively chaotic. Once the proprietary AMM optimized transaction efficiency and Hyperliquid siphoned off high-value orders, this profit quickly shrank. While L1 can make a significant profit during market frenzy, the market will quickly find new ways to prevent this short-term gain from continuing indefinitely.

Impact on Token Prices

The pattern exhibited by the three chains mentioned above is not just a retrospective description; to some extent, it also has foresight. Every L1 fee mechanism follows the same trajectory: new demand brings peak revenue, the peak attracts innovation, innovation compresses profits, and once this compression occurs, it is challenging to reverse. Following this line of thought, we can have a rough judgment on the future of the four tokens.

· Ethereum: Sustained fee "collapse"

Ethereum's fees have not yet seen a clear bottom. In 2024, L2 contributed $113 million to the Ethereum mainnet; by 2025, it plummeted to around $10 million, a decrease of over 90%. With each new L2, the demand for Ethereum mainnet block space decreases, and Ethereum's own scaling plans continue to lower the cost of data transmission. EIP-4844 is not a one-time repricing but a structural shift—Ethereum is proactively diverting activity away from its fee market to infrastructure tools outside it.

Currently, monthly L1 fee revenue has dropped below $15 million, and the forces driving the decline are still strengthening. If Ethereum cannot create entirely new L1 native demand sources, the token price will continue to reflect this compression trend. ETH is increasingly resembling a low-yield infrastructure asset rather than the high-growth smart contract platform it once was.

· Solana: Peak Activity Innovation, Price Not Necessarily

Solana is almost certain to set a new peak in on-chain activity in the next cycle — its ecosystem is deep enough, with plenty of developers, and its infrastructure mature enough. However, fee revenue may not rise accordingly. The meme coin frenzy from late 2024 to early 2025 was Solana's equivalent of Bitcoin's "SegWit moment": a peak in fees driven by new demand, followed by rapid compression due to innovation.

Currently, proprietary AMMs have processed over 50% of DEX trading volume, significantly mitigating MEV. Hyperliquid's HyperCore technology is even moving the most profitable pricing stages off-chain. Even if on-chain activity is 2 to 3 times higher than in January 2025, its fee system has matured to the point where it is quite challenging to translate this activity into corresponding validator revenue. Despite a drop of over 90% in daily average MEV fees from its peak, on-chain activity remains robust. Without sufficient fee revenue to support its valuation, even if Solana's adoption reaches new highs, the possibility of SOL breaking its all-time high in the next cycle is slim.

· Hyperliquid: Prosperity and Compression of the Front and Backends

Hyperliquid is the most noteworthy case as it represents the next stage of this "earn-squeeze" cycle, and the market has yet to realize how the latter part of this cycle will unfold.

Hyperliquid is now the leading decentralized exchange for traditional financial asset perpetual contract (perps) trading. During a recent silver volatility peak, the market deployed by HIP-3 captured about 2% of global silver trading volume, with the midpoint spread for retail-scale trades even outperforming COMEX. At certain times, traditional financial instruments accounted for about 30% of platform trading volume, with daily nominal trading volume exceeding $5 billion. The platform's revenue in 2025 was about $600 million, 97% of which was used for HYPE token buybacks and burns.

We expect Hyperliquid to continue dominating perpetual contract trading for TradFi assets. Its products do have advantages: commodities and stocks can be traded 24/7, even when traditional markets are closed; through the HIP-3 proposal, new trading markets can be added without approval; for assets requiring an 18% initial margin on CME, it can offer up to 20x leverage. In the next bull market, if trading volume and fees continue to rise, the HYPE token may reprice like Solana did from the bear market low point, if traditional financial asset trading volume keeps expanding, HYPE will likely follow a similar path. Investors are likely to use a single high revenue quarter to project that it will continue to earn as much in the future.

However, Hyperliquid's fee model has planted a compressed seed. The platform charges a nominal value fee of 4.5 basis points to the maker and offers up to a 40% discount based on trading volume and staking. This is in stark contrast to traditional financial derivative pricing logic. At the CME, the exchange fee for one E-mini S&P 500 contract is about $1.33 per side, unrelated to the nominal value above $275,000, equivalent to less than 0.001 basis points. For a $10 million nominal position: CME fees are about $2.50, while Hyperliquid charges $4,500, a difference of approximately 1,800 times.

This price differential exists because Hyperliquid's current user base is primarily retail and crypto-native. However, TradFi perpetual products will bring TradFi expectations. As trading volume expands and institutional participants enter, the pressure to move closer to a CME-like economic model will significantly increase. Hyperliquid's own fee structure has revealed the direction: HIP-3 growth mode will cut maker fees for new markets by over 90%, potentially as low as 0.0045%; top traders may even go below 0.0015%. The protocol is actively driving fee compression. Competitive perpetual DEXs, as well as traditional exchanges offering on-chain products in the future, will further accelerate this process.

Ultimately, there are only two outcomes: either Hyperliquid loses trading volume due to high fees, or it adjusts its fee structure to a fixed fee model similar to CME's. Either way, the long-term high revenue that investors are currently anticipating will be challenging to achieve, and the HYPE token price may also experience a rapid decline.

· Bitcoin: Price Must Rise Before Fees

Among these four assets, Bitcoin is the most unique, as its fee and token price have a reversed logic relationship. For Ethereum, Solana, and Hyperliquid, the logic is: fees generate revenue, revenue supports valuation, fees get compressed, and token prices drop. But Bitcoin is different; the logic is reversed. Miners must rely on a continuous increase in coin price to survive each block reward halving because fee revenue has been proven insufficient to make up for the reduced block subsidy.

The 2024 halving will reduce block rewards from 6.25 BTC to 3.125 BTC, and the daily issuance will drop from 900 BTC to 450 BTC. By the end of 2025, daily transaction fees will be about $300,000, accounting for less than 1% of miner revenue. Although Bitcoin's full-year fee revenue in 2024 reached $922 million, most of it came from the phase-related peaks of Ordinals and Runes, rather than sustainable natural fee demand. Current fee contributions are almost negligible, and miner revenue relies almost entirely on block subsidies, which halve every four years, based on BTC pricing. The only way miners can remain profitable during the halving cycle is if Bitcoin's USD price roughly doubles over a similar timeframe to offset the 50% reduction in BTC-denominated income.

In history, this condition has been met. However, this foundation is extremely fragile. The security budget of the chain is not funded by usage but by the continuous rise in asset price. Once at a halving event, if the coin price does not increase, mining will become unprofitable, hash rate will decrease, network security will be affected, and it may even fall into a vicious cycle of "price drop → hash rate drop → decreased security → further price drop".

This also makes Bitcoin's "sustainability" more fragile than it seems. The coin price can support network security with almost no transaction fees, a mechanism that other chains find hard to replicate, because Bitcoin is primarily an asset currency, not a smart contract platform.

People buy BTC to hold it, not to use its block space. This gives Bitcoin an advantage that other chains don't have: Relying on everyone's demand for the currency to drive price increases, even with very low transaction fees, can still maintain network security.

However, this also means that Bitcoin's long-term security relies entirely on one assumption—that the price of the coin will always rise, a guarantee that no one can provide. Whether this chain can continue to act as a secure settlement layer does not depend on whether it can develop applications that earn transaction fees but on whether it can continuously maintain the narrative and market environment that make everyone willing to buy BTC. So far, this model has been operating normally, but when the block subsidy further reduces from 3.125 BTC to 1.5625 BTC, 0.78125 BTC, and in the future, three to four more halvings, whether it can fill the gap through price increases will be the most critical unknown in the crypto space.

You may also like

AI Crypto Trading Bot Explained: Aurora's Multi-Factor Strategy in WEEX Hackathon

Aurora demonstrates how structured, multi-agent AI Trading systems can deliver more adaptive and resilient performance in the WEEX AI Trading Hackathon.

Cyber Taoist Fortune Teller: Fake Taoist, AI Fortune Telling, and Northeastern Metaphysics History

Bloomberg: Stablecoin Payments Emerge as Crypto VC's Newest Favorite Thing

BeatSwap is evolving towards a full-stack Web3 infrastructure, covering the entire lifecycle of IP rights.

BeatSwap, a global Web3 Intellectual Property (IP) infrastructure project, is attempting to overcome the current fragmentation limitations of the Web3 ecosystem, building a full-stack system that covers the entire lifecycle of IP rights.

Currently, most Web3 projects are still in the stage of functional fragmentation, often focusing only on a single aspect, such as IP asset tokenization, transaction functionality, or a simple incentive model. This structural dispersion has become a key bottleneck hindering the industry's scale application.

BeatSwap's approach is more integrated, integrating multiple core modules into the same system, including:

· IP authentication and on-chain registration

· Authorization-based revenue sharing mechanism

· User-engagement-driven incentive system

· Transaction and liquidity infrastructure

Through the above integration, the platform builds an end-to-end closed-loop path, allowing IP rights to complete a full cycle of "creation, use, and monetization" within the same ecosystem.

BeatSwap is not limited to existing crypto users but is attempting to take the global music industry as a starting point, actively creating new market demand. Its core strategies include:

Exploring and incubating music creators (Artist discovery)

Building a fan community

Igniting IP-centric content consumption demand

The current global music industry is valued at around $260 billion, with over 2 billion digital music users. This means that the potential market corresponding to the tokenization and financialization of IP far exceeds the traditional crypto user base.

In this context, BeatSwap positions itself at the intersection of "real-world content demand" and "on-chain infrastructure," attempting to bridge the structural gap between content production and financial flow.

BeatSwap's upcoming core product "Space" is scheduled to launch in the second quarter of 2026. This product is defined as the SocialFi layer in the ecosystem, aiming to directly connect creators with users and achieve deep integration with other platform modules.

Key designs include:

A fan-centric interactive mechanism

Exposure and distribution logic based on $BTX staking

User paths connected to DeFi and liquidity structures

Thus, a complete user behavior loop is formed within the platform: Discovery → Participation → Consumption → Rewards → Trading

$BTX is designed to be a core utility asset within the ecosystem, rather than just a simple incentive token, with its value directly tied to platform activity and IP use cases.

Main features include:

· Yield distribution based on on-chain authorized actions

· Value reflection based on IP usage and user engagement dynamics

· Support for staking and DeFi participation mechanisms

· Value growth driven by ecosystem expansion

With the increased frequency of IP use, the utility and value support of $BTX will enhance simultaneously, helping alleviate the "disconnect between value and utility" issue present in traditional Web3 token models to some extent.

Currently, $BTX has been listed on several mainstream exchanges, including:

Binance Alpha

Gate

MEXC

OKX Boost

As the launch of "Space" approaches, BeatSwap is actively pursuing more exchange listings to further enhance liquidity and global accessibility, laying a foundation for future market expansion.

BeatSwap's goal is no longer limited to the traditional Web3 narrative but aims to target over 2 billion digital music users and a trillion KRW-scale content market.

By integrating content creators, users, capital, and liquidity into a blockchain framework centered around IP rights, BeatSwap is striving to build a next-generation infrastructure focused on "IP tokenization."

BeatSwap integrates IP authentication, authorization distribution, incentive mechanism, transaction system, and market construction to establish a unified structure that bridges the full lifecycle path of IP rights.

With the launch of the Q2 2026 "Space," the project is expected to become a key infrastructure connecting content and finance in the IP-RWA (Real World Assets) track.

Mag 7 Evaporates $2 Trillion | Rewire News Morning Edition

Losing $19K per Coin Mined, Bitcoin Mining Firms Collective AI Defection

Morning Report | Tom Lee predicts that the cryptocurrency winter will end in April; xStocks introduces a new on-chain private equity fund; Sui mainnet upgraded to V1.68.1

Polymarket rules have changed, how should airdrop participants respond?

Crypto ETF Weekly | Last week, the net outflow of Bitcoin spot ETFs in the U.S. was $296 million; the net outflow of Ethereum spot ETFs in the U.S. was $206 million

This Week's Key News Preview | The U.S. Releases March Non-Farm Payroll Data; Polymarket Expands Fee Structure

Slow Down, That's the Answer to the Age of the Agent

From Cash to Cryptocurrency: Moving Towards a Unified Regulatory Path for Illegal Payments

Who will own the most Bitcoin in 2026

A private feud lasting 10 years, if not for OpenAI's "hypocrisy," would not have led to the world's strongest AI company, Anthropic

"Crypto Tsar" steps down: 130 days of political performance come to an end, how much of Trump's crypto promise remains?

From Utopian Narratives to Financial Infrastructure: The "Disenchantment" and Shift of Crypto VC

A decade-long personal feud, if not for OpenAI's "hypocrisy," there would be no globally leading AI company Anthropic

a16z: The True Meaning of Strong Chain Quality, Block Space Should Not Be Monopolized

AI Crypto Trading Bot Explained: Aurora's Multi-Factor Strategy in WEEX Hackathon

Aurora demonstrates how structured, multi-agent AI Trading systems can deliver more adaptive and resilient performance in the WEEX AI Trading Hackathon.

Cyber Taoist Fortune Teller: Fake Taoist, AI Fortune Telling, and Northeastern Metaphysics History

Bloomberg: Stablecoin Payments Emerge as Crypto VC's Newest Favorite Thing

BeatSwap is evolving towards a full-stack Web3 infrastructure, covering the entire lifecycle of IP rights.

BeatSwap, a global Web3 Intellectual Property (IP) infrastructure project, is attempting to overcome the current fragmentation limitations of the Web3 ecosystem, building a full-stack system that covers the entire lifecycle of IP rights.

Currently, most Web3 projects are still in the stage of functional fragmentation, often focusing only on a single aspect, such as IP asset tokenization, transaction functionality, or a simple incentive model. This structural dispersion has become a key bottleneck hindering the industry's scale application.

BeatSwap's approach is more integrated, integrating multiple core modules into the same system, including:

· IP authentication and on-chain registration

· Authorization-based revenue sharing mechanism

· User-engagement-driven incentive system

· Transaction and liquidity infrastructure

Through the above integration, the platform builds an end-to-end closed-loop path, allowing IP rights to complete a full cycle of "creation, use, and monetization" within the same ecosystem.

BeatSwap is not limited to existing crypto users but is attempting to take the global music industry as a starting point, actively creating new market demand. Its core strategies include:

Exploring and incubating music creators (Artist discovery)

Building a fan community

Igniting IP-centric content consumption demand

The current global music industry is valued at around $260 billion, with over 2 billion digital music users. This means that the potential market corresponding to the tokenization and financialization of IP far exceeds the traditional crypto user base.

In this context, BeatSwap positions itself at the intersection of "real-world content demand" and "on-chain infrastructure," attempting to bridge the structural gap between content production and financial flow.

BeatSwap's upcoming core product "Space" is scheduled to launch in the second quarter of 2026. This product is defined as the SocialFi layer in the ecosystem, aiming to directly connect creators with users and achieve deep integration with other platform modules.

Key designs include:

A fan-centric interactive mechanism

Exposure and distribution logic based on $BTX staking

User paths connected to DeFi and liquidity structures

Thus, a complete user behavior loop is formed within the platform: Discovery → Participation → Consumption → Rewards → Trading

$BTX is designed to be a core utility asset within the ecosystem, rather than just a simple incentive token, with its value directly tied to platform activity and IP use cases.

Main features include:

· Yield distribution based on on-chain authorized actions

· Value reflection based on IP usage and user engagement dynamics

· Support for staking and DeFi participation mechanisms

· Value growth driven by ecosystem expansion

With the increased frequency of IP use, the utility and value support of $BTX will enhance simultaneously, helping alleviate the "disconnect between value and utility" issue present in traditional Web3 token models to some extent.

Currently, $BTX has been listed on several mainstream exchanges, including:

Binance Alpha

Gate

MEXC

OKX Boost

As the launch of "Space" approaches, BeatSwap is actively pursuing more exchange listings to further enhance liquidity and global accessibility, laying a foundation for future market expansion.

BeatSwap's goal is no longer limited to the traditional Web3 narrative but aims to target over 2 billion digital music users and a trillion KRW-scale content market.

By integrating content creators, users, capital, and liquidity into a blockchain framework centered around IP rights, BeatSwap is striving to build a next-generation infrastructure focused on "IP tokenization."

BeatSwap integrates IP authentication, authorization distribution, incentive mechanism, transaction system, and market construction to establish a unified structure that bridges the full lifecycle path of IP rights.

With the launch of the Q2 2026 "Space," the project is expected to become a key infrastructure connecting content and finance in the IP-RWA (Real World Assets) track.