Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Overseas VC's Two-Week Trip to China AI Leaves Them in Awe of Shenzhen Hardware

Original Title: What I Learned from Two Weeks Inside China's AI Ecosystem

Original Author: José Maria Macedo, Co-founder of Delphi Labs

Original Translation: DeepFlow Tech

DeepFlow Summary: The founder of Delphi Labs spent two weeks extensively exploring China's AI ecosystem, meeting numerous founders, investors, and CEOs of listed companies.

His conclusion was unexpected: more bullish on hardware than anticipated, more bearish on software than expected, and his observations of Chinese founders challenged his previous assumptions.

The article also covers topics such as valuation bubbles, the humanoid robot race, and the information asymmetry between the East and the West.

Full Text:

I spent two weeks in China, meeting a large number of founders, VCs, and CEOs of AI companies. Before going, I was bullish on this ecosystem, expecting to see world-class AI talent working at valuations far below those in the West.

My view changed when I left — in more nuanced ways: hardware is stronger than I expected, software is weaker than I expected, and some observations about Chinese founders surprised me.

Founder Issues

One common trait among exceptional founders I have backed is: independent thinking, rebelliousness, extreme focus, and passion. They don't follow the rules. They keep asking "why," refusing to accept secondhand wisdom. The decisions they make, seemingly inexplicable to others, seem perfectly logical to them. They possess an inherent, unstoppable intensity, often manifested as a long-term obsession with excellence. As a VC, encountering numerous intelligent individuals daily, these individuals stand out in a crowd because their life trajectories exhibit a distinct "sharpness."

Many founders I met in China belong to a different category, which surprised me.

They are exceptionally accomplished — graduates from top universities, with backgrounds at companies like ByteDance or DJI, publications in Nature, and multiple patents. In the West, these achievements are only seen in the most elite technical talent, but in China, they are entry-level requirements. They also work harder than almost everyone I have met. We had meetings at all hours, including weekends, and rushed between cities. One founder even came to see us on the day his wife was giving birth.

However, independent thinking, a rebellious spirit, and a vision from 0 to 1 are harder to find. The founders' backgrounds are highly similar, the pitches are more conservative, many ideas are upgrades of existing products (impressive V2), rather than truly original bets. With such a large number of tech talent coming from China, I originally expected to encounter more people presenting "ideas I've never heard of before."

My interpretation is: China's education system nurtures excellence but does not leave enough room for deviation. It produces top-notch executors who excel at solving known problems, rather than individuals who "bring forth a problem that no one knew existed."

VC Reinforcing This Pattern

What's even more interesting is how local investors are exacerbating this trend.

The investment logic of most Chinese funds is built on one premise: investing in the most outstanding individuals who have come out of ByteDance or DJI. They look at resumes, not sharpness; at background, not beliefs. The VCs themselves fit this mold — coming from large corporations or consulting and investment banking backgrounds, similar to European VCs from ten years ago.

Ironically, most of the Chinese founders who have truly built great companies have never worked in a large corporation. Jack Ma was an English teacher who took the college entrance exam twice to get in. Ren Zhengfei founded Huawei at the age of 43, with a background in the military. Liu Qiangdong started by selling goods at a trading market. Dr. Wang Xing began his entrepreneurial journey without completing his doctorate. Most recently, William Li, who founded DeepSeek, has never worked outside his own company. These individuals are outliers, part of the group without a "standard resume" — precisely the kind of people the current investment system will overlook.

Finding these individuals yields real alpha, but currently, it seems few are looking there.

Shenzhen and the Hardware Ecosystem

The most awe-inspiring thing I saw in China was not the pitch of any startup.

It was the hardware underground workshops in Shenzhen — engineers systematically acquiring Western high-end products, dismantling them part by part, and reverse-engineering everything in an extremely meticulous way. When I stepped out, I was truly unsure if most Western hardware founders understand who they are competing against. The network effects here are not theoretical; they are physical, dense, and have been accumulated over decades.

The entrepreneurs we met validated this with data: over 70% of hardware inputs come from the Greater Bay Area, nearly 100% from China itself — this means the iteration cycle is something Western hardware companies simply cannot match.

Most founders I've seen are using DJI's playbook: focusing on a specific niche to build consumer hardware—electric wheelchairs, lawn mowing robots, next-gen fitness equipment—scaling revenue to 8 to 9 digits (USD), then leveraging their customer base or underlying technology to expand into adjacent categories. Some companies have grown much larger than you'd imagine. The most impressive company I've seen this time is Bambu Lab, a 3D printing company that most Westerners haven't heard of, reportedly generating $500 million in annual profit and doubling their revenue every year.

Bearish on Chinese Software

When I left, my skepticism about the opportunities in Chinese software had deepened compared to when I arrived.

At a model level, China's open source ecosystem is indeed strong, but the closed-source models still lag significantly behind the best in the West, and the gap may be widening. The capital expenditure gap is immense. GPU access remains restricted. Western labs are increasingly cracking down on distillation. Revenue numbers tell the tale: Anthropic reportedly hit $6 billion in ARR in February alone. The top Chinese model companies are in the tens of millions of dollars range for ARR.

In the software startup realm, the mainstream profile is ByteDance alumni turned PMs and researchers building agentic or ambient consumer software targeting Western markets. The talent is indeed strong, but many of these products happen to fall within the range of native functionality that large labs might release—an update could render them obsolete. What's also surprising to me is that China lacks large, rapidly growing private software companies. In the West, apart from model companies, there's a cohort of startups already hitting 9 or even 10 digits in ARR, with astounding growth rates—Cursor, Loveable, ElevenLabs, Harvey, Glean. This breakthrough level of private software companies is basically nonexistent in China—few exceptions like HeyGen, Manus, GenSpark have emerged, but they've all exited after starting up.

Valuation Bubble

Despite the unimpressive software landscape, there's a tangible bubble—both in early and late stages.

Looking at the early stage, the most elite talent coming out of ByteDance, DeepSeek, DarkSide of the Moon, indeed costs significantly less than equivalent-level American talent, but the median valuations have converged. Consumer startups without products are commonly valued at $100-200 million. Seed rounds exceeding $30 million are not uncommon.

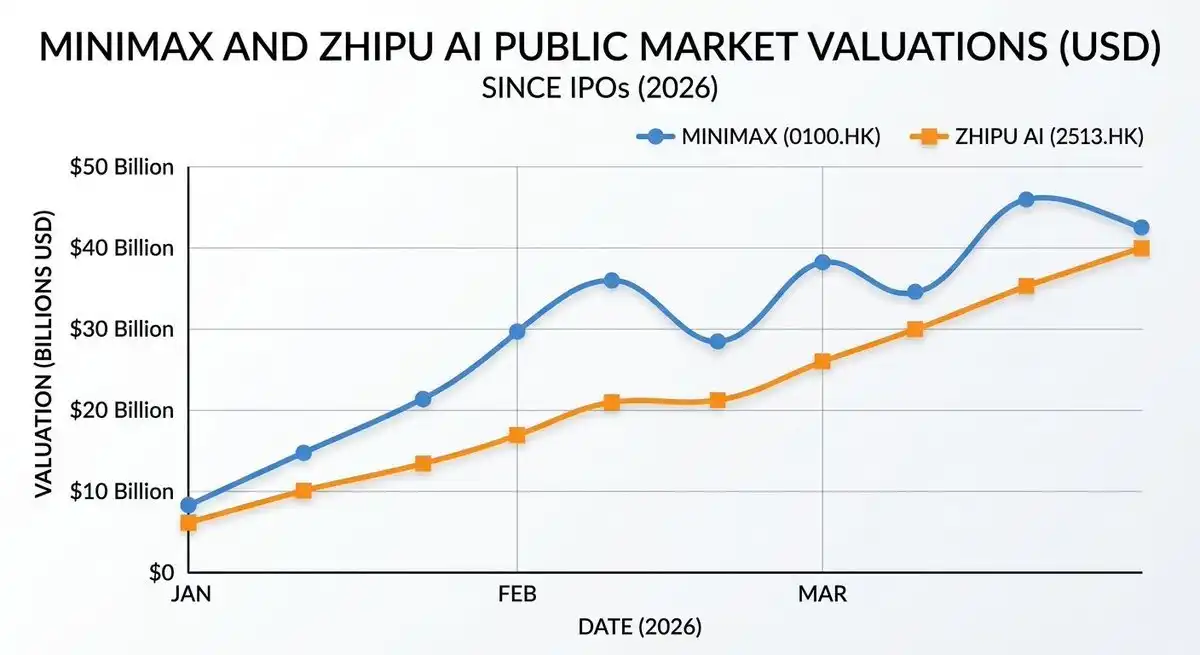

Late-stage digital is increasingly hard to justify. MiniMax is valued at around $40 billion in the public markets, with less than $100 million in ARR—roughly 400x revenue. Wisdom Spectrum is around $25 billion in valuation with $50 million in revenue. For comparison: OpenAI's highest valuation round was roughly 66x ARR, Anthropic around 61x.

The dark side of the Moon and other private model companies are using these public market comparables to fundraise—going from $6 billion to $10 billion in a few months to $18 billion. Crypto-savvy friends will recognize this pattern well: Investors use the private valuation as a benchmark against a "pre-unlock" public market price. Furthermore, Wisdom Spectrum and MiniMax can sustain these levels, in part because they are currently the only way to get exposure to the "China AI narrative," which has its own premium.

But as more companies go public, this premium will get diluted. Lastly, the IPO window has a unique feature—it can close suddenly without warning. No one can guarantee you'll have time to unwind this arbitrage before the benchmark price moves.

The humanoid robot race is in a similar situation. China has about 200 humanoid robot companies, with around 20 raising over $100 million, several valued at several billion—almost all with no revenue, and most planning for an IPO on the Hong Kong Stock Exchange in 2026 or 2027. If this market is real, China's hardware advantage sets a relatively clear long-term trajectory. However, commercialization may take much longer than the current fundraising pace suggests, and I doubt the Hong Kong Stock Exchange can handle the many multi-billion-dollar humanoid robot companies currently queued up for IPO. I'm staying away for now.

Image: Couldn't resist sharing a video of a humanoid robot performing a front flip

Notable Information Asymmetry

One thing surprised me: Almost every founder I've met is first targeting the global market before considering China. They use Claude Code, watch Dwarkesh's podcast, and have an in-depth knowledge of the San Francisco startup ecosystem—often more so than Western investors who haven't been paying attention.

Western animosity towards China is significantly greater than Chinese animosity towards the West. Chinese founders do not see a contradiction in combining China's execution capabilities and hardware depth with Western go-to-market and product thinking. When this combination takes shape within a suitable founding team, truly remarkable companies are born.

Identifying these founders — those who do not fit the "standard resume template" optimized by the local VC system — is what we are doing now.

A special thanks to @woutergort for opening up his excellent Chinese network, @PonderingDurian for organizing this trip, and to Claude for patiently editing my ramblings on the plane.

You may also like

The most important thing in Web3 primary market investment

The strategic focus of cryptocurrency in reconstructing the international monetary system and the Chinese solution

Musk Poached Aave App's Web3 Prodigy

The Petro Order is Cracking. What Comes Next for the Middle East?

ETF Fund Inflows Emerging, What's Still Missing for BTC to Fully Recover?

Forbes Special Report: The Embrace of AI Agents in the Cryptocurrency Industry

Bitpanda, Vision Web3 Foundation, and Optimism Partner to Onboard European Financial Institutions to the Global Blockchain Economy

What will the early Hyperliquid prediction market look like?

Was CZ Also Rug Pulled? BNB Treasury CEA Industries Control Battle

A transaction in 7 seconds, earning tens of millions of dollars, he's seen as the "cancer of meme coins."

Bittensor Ecosystem Token SN Surges 5x in March, What's Behind Richard Heart's One-Liner?

The economy is entering a new cycle, how can the average person prepare?

Access Binance Alpha Box: Sigma.Money to Launch BNB Chain Ecosystem Yield Farming Gateway

Kimi, Chip, and Bean come together for a Crypto Hackathon: What did AI developers build on Monad?

How to Trade Crypto on Mobile Browser & Win LALIGA Tickets (2026 Guide)

Discover how AI automation, natural language trading, and mobile browser trading platforms are shaping automated trading in 2026. Join the WEEX live trading event for early access and rewards like LALIGA VIP tickets.

Connecting encryption, TradFi, and payments, is Gate completing the final puzzle of the "super APP"?

a16z Crypto Operating Partner: Wall Street is undergoing its biggest infrastructure upgrade in 30 years