Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

The Circle Beautiful Money Report: Is the True Winner of Stablecoins Not the Issuer?

Original Title: Circle's $461M payout shows who captures USDC yield—and it's not Circle

Original Author: Gino Matos, CryptoSlate

Original Translation: TechFlow at DeepTech

DeepTech Summary: Circle's Q4 data looks promising — USDC scale up 72% YoY, yield quintupled — but the financials reveal a harsh reality: for every $1 earned in reserve yield, $0.63 flows to gatekeeping exchanges and wallet channel providers. This article delves into the yield distribution structure, analyzing the power play between the stablecoin issuer, channel providers, and users, and how this system will come under pressure as interest rates decline.

Full Text:

Circle's Q4 report tells a growth-oriented story the company hopes investors will understand: USDC circulation grew 72% YoY to $75.3 billion, reserve yield surged 69%, and adjusted EBITDA grew fivefold.

However, the income statement presents a different picture — the issuer generates revenue only to promptly cede most of it to platforms controlling user access.

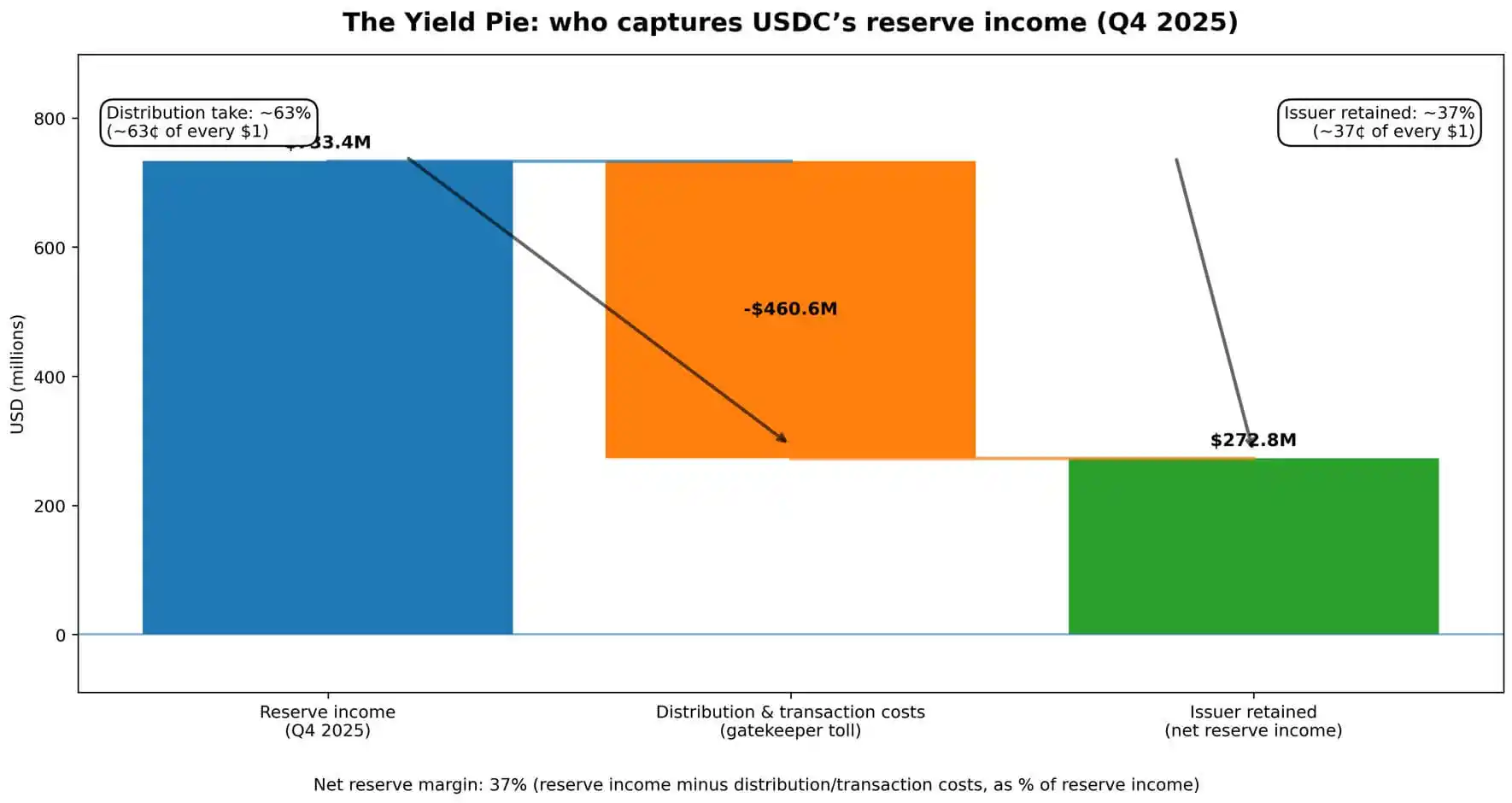

The numbers speak for themselves. Circle's quarterly reserve yield was $733.4 million.

Of this, $460.6 million was distributed and consumed as trading costs, roughly $0.63 from every $1 earned siphoned off — funds stemming from investing customer deposits.

Total revenue combined with reserve yield amounted to $770.2 million, with distribution costs representing almost 60% of all revenue flowing through the company's operations.

What Circle is left with is what remains after paying off the "gatekeepers."

This is not information hidden in the footnotes. Circle presents the "Revenue Less Distribution Costs" (RLDC) as a key performance indicator, disclosing the RLDC profit margin quarterly alongside earning data and net revenue.

The message conveyed to investors is: revenue is there, but to access it, one must pay the "shelf fee." The essence of the stablecoin business is a negotiation between the issuer and the gatekeeping exchanges, wallets, and fintech channels that effectively own the controlled balance.

Who Shares the Revenue Cake

A stablecoin generates revenue through a direct mechanism.

Users deposit dollars or convert cryptocurrency into a stablecoin. The issuer holds these funds in reserve, primarily invested in short-term government securities and similar instruments, earning the current interest rate.

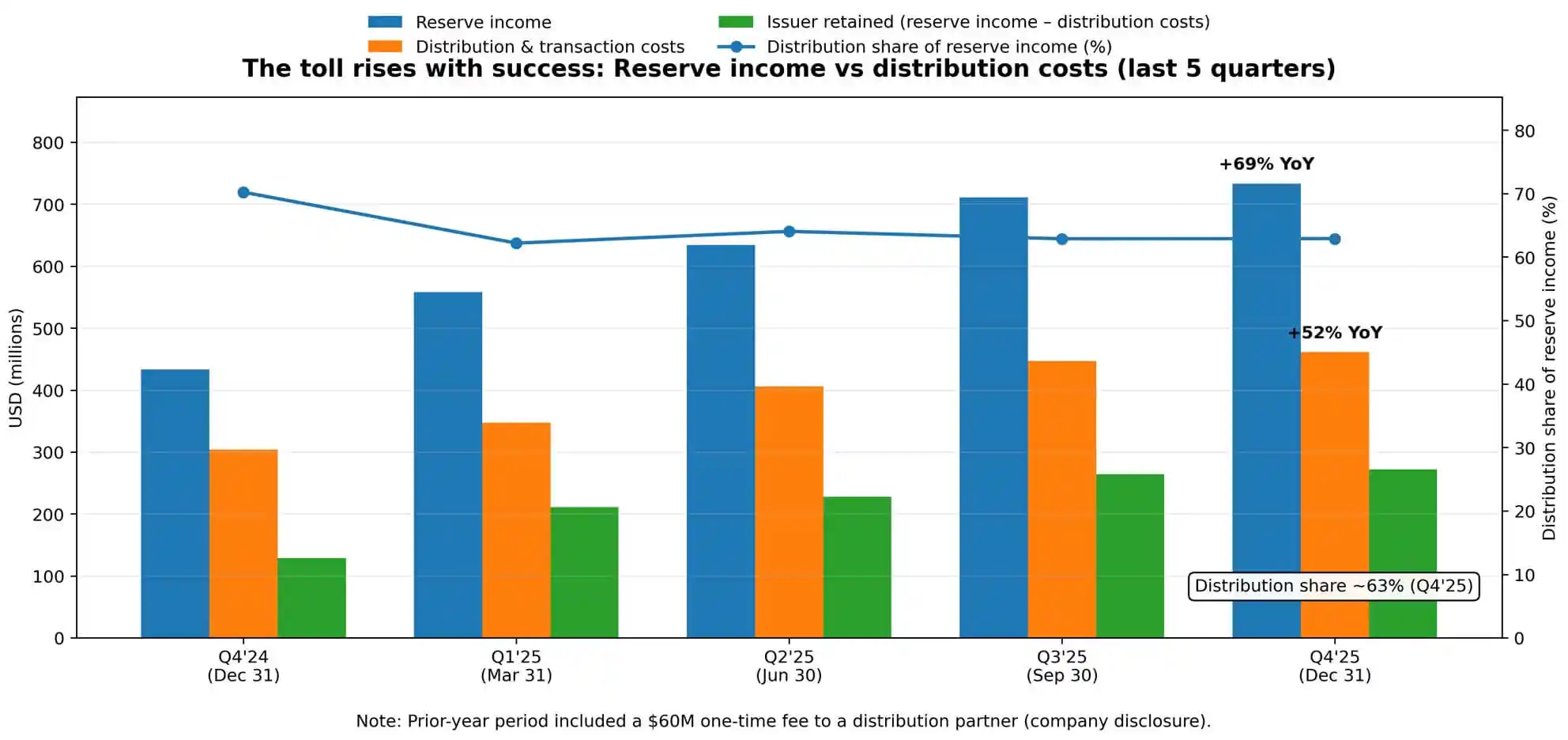

Circle's Q4 Reserve Report shows a return rate of 3.8%, down 68 basis points year-on-year, reflecting the evolution of the Fed's path. But even as interest rates decline, reserve revenue continues to climb — as the average USDC circulation doubles from $38.1 billion to $76.2 billion.

Scale outweighs rate. This dynamic is key to understanding the 52% year-on-year increase in distribution costs.

Circle explicitly attributes this growth to "increased distribution payments," noting that the prior year period included a disclosed $60 million one-time expense.

Excluding this one-time payment, the intrinsic growth of the distribution economy accelerates further. The bigger the cake, the faster the tolls rise.

Circle's net reserve profit margin — the reserve revenue minus distribution and transaction costs as a percentage of reserve revenue — remained steady at 37% in Q4.

In other words, for every $1 of total reserve revenue earned, Circle retains about $0.37, with the rest flowing to distribution partners.

This cost structure is not easily diluted as scale increases.

Distribution payments are not technology expenses, nor are they fixed costs that can be diluted with transaction volume. They are negotiated economic arrangements tied to channel positions and fund flows, meaning they are sticky and may rise further as the bargaining power of the "gatekeepers" strengthens.

Distribution "Oligopoly" Structure as Market Framework

The term "oligopoly" here is metaphorical, not accusatory. It refers to a few gatekeepers controlling user access points, extracting a proportionate share of economic benefits based on their bargaining power.

Circle's own risk disclosures make this point clear. The company warns that it may "be unable to maintain existing relationships with financial institutions and similar businesses," or establish new ones. It also highlights the risk of accepting "less favorable financial terms" and that "reliance on a few key distributors" is a structural constraint.

These terms are crucial as they position the distribution relationship as a power play rather than a vendor relationship. Circle reported a metric called "USDC on Platforms," tracking the proportion of USDC held on partner platforms to the total supply.

This figure reached $12.5 billion by year-end, a 459% year-on-year increase, with a daily weighted average representing 17.8% of total circulation. The company actively monitors where balances concentrate — once again affirming: Whoever controls the channel dictates who captures the value.

The battleground of competition is not stablecoin technology or reserve management but rather access.

Exchanges, wallets, and payment platforms sit between the issuer and the user, monetizing this position. Circle can build better products, gain regulatory clarity, and optimize reserve returns.

However, if a major distributor changes incentives or threatens to promote a competitor, the economic landscape could quickly reverse. The issuer's profit margins hinge on the terms set by gatekeepers.

What Happens in a Declining Rate Environment

Currently, this system operates in an environment with a median interest rate of around 3%, where the yield on the reserve portfolio is sufficient to support both the issuer and distributors' economic interests, leaving room for margin expansion.

But interest rates have direction, and the Fed's path is crucial. As of late February 2026, the Treasury bond yield anchoring the reserve portfolio rate remains within the 3% median range. However, the market anticipates potential rate cuts in the coming quarters.

In a declining rate environment, if distribution costs are sticky, the issuer's economic pressure will increase more rapidly than the decline in distributor cuts.

In a potential scenario, if rates fall by 100 basis points, and distribution payments remain fixed or decrease at a slower pace than reserve earnings, Circle's RLDC profit margin will face further pressure.

If rates drop another 100 basis points, under sticky distribution contracts, the issuer's economics may approach zero or even turn negative, prompting renegotiation or industry consolidation.

This is not speculation. Circle's guidance has already reflected an expected margin compression relative to a Q4 40% RLDC profit margin. The company is pricing in a world where distribution costs do not decrease proportionally to reserve earnings.

This dynamic intensifies the competition for the remaining spread, driving the entire category towards more aggressive "pay-to-play" arrangements or structural resets.

The Political Economy of Floating Reserves

A stablecoin presents an unusual political-economic arrangement.

Users provide floating reserves—$75 billion in Circle's case—but in most implementations, users do not earn a direct yield. The issuer earns the reserve yield but passes most of the share to distributors. Distributors capture economic value through control of access but do not bear asset-liability risk.

As long as users value convenience and stability over yield, this setup can function. However, once stablecoins reach mainstream scale, the question of who should receive this yield becomes increasingly hard to avoid.

The "GENIUS Act" is referenced in Circle's disclosures as legislation relevant to its regulatory environment. As the regulatory framework formalizes, the question of who should receive the yield will become harder to sidestep.

If stablecoins are serving as a deposit substitute, why shouldn't users earn interest? If they are payment rails, what justifies gatekeepers claiming such a sizeable economic share? If they are reserve assets, why can't the issuer retain a larger spread?

These are not rhetorical questions but the basis for renegotiation between issuers and distributors, platforms and users, industry and regulators in the future.

Circle's current profit margin structure reflects its bargaining power at a specific moment. This power will shift with changes in market share, regulatory posture, and alternative channels.

The Real Risk Is Not a Bank Run

Circle's balance sheet can withstand a large-scale redemption shock. The reserves are liquid, audited, and managed conservatively.

The operational risks disclosed by the company are not in the classical sense of a bank run but distributor switching—a major partner changing incentives, promoting a competitor, or building stablecoin infrastructure in-house.

This form of risk is fundamentally different from credit or liquidity risk. It is a market structure risk related to how stablecoins reach users.

If a top-tier exchange decides to prioritize support for another stablecoin, fund flows would quickly change. If a fintech platform integrates a competitor's channel, the distribution economy would reshuffle.

The issuer's options are limited: pay more to retain channel placement, accept margin compression, or build a direct-to-user distribution channel in-house—which is a capital-intensive, time-consuming alternative path.

Circle's "On-Platform USDC" metric exists because the company needs to monitor this concentration.

Where balances concentrate is where bargaining leverage resides. The more USDC is concentrated on a particular platform, the more that platform can extract in negotiations.

The issuer's profit margin is the remaining balance claim after distribution partners take their share.

Endgame Issue

The shape of stablecoin competition is akin to a bidding war for channels.

Market share capture relies not on technical or regulatory advantages but on establishing and maintaining distribution relationships.

This structure benefits issuers with capital to pay channel fees and distributors with a large enough user base to drive economies of scale.

The integration pressure is evident.

Interest rate downsides compress issuer margins. As distributors can negotiate better terms from concentrated relationships, their willingness to support multiple stablecoins decreases. Users gravitate towards defaults embedded in platforms they already use.

The entire category trends towards fewer issuers, stronger distributors, and as the revenue pie shrinks, both sides' margins are under pressure.

Circle's Q4 embodies what this logic looks like at scale.

The company generated $733 million in reserve revenue and paid $461 million to secure user access. The issuer retained $272 million leftover before deducting operational expenses.

This is the economic reality of stablecoins: they are not just digital dollars or interest rate trades.

They represent a negotiation between the issuer and gatekeepers over who captures the spread—a quarterly affair, with the stakes of this game determined by float size and rate levels.

You may also like

Cyber Taoist Fortune Teller: Fake Taoist, AI Fortune Telling, and Northeastern Metaphysics History

Bloomberg: Stablecoin Payments Emerge as Crypto VC's Newest Favorite Thing

BeatSwap is evolving towards a full-stack Web3 infrastructure, covering the entire lifecycle of IP rights.

BeatSwap, a global Web3 Intellectual Property (IP) infrastructure project, is attempting to overcome the current fragmentation limitations of the Web3 ecosystem, building a full-stack system that covers the entire lifecycle of IP rights.

Currently, most Web3 projects are still in the stage of functional fragmentation, often focusing only on a single aspect, such as IP asset tokenization, transaction functionality, or a simple incentive model. This structural dispersion has become a key bottleneck hindering the industry's scale application.

BeatSwap's approach is more integrated, integrating multiple core modules into the same system, including:

· IP authentication and on-chain registration

· Authorization-based revenue sharing mechanism

· User-engagement-driven incentive system

· Transaction and liquidity infrastructure

Through the above integration, the platform builds an end-to-end closed-loop path, allowing IP rights to complete a full cycle of "creation, use, and monetization" within the same ecosystem.

BeatSwap is not limited to existing crypto users but is attempting to take the global music industry as a starting point, actively creating new market demand. Its core strategies include:

Exploring and incubating music creators (Artist discovery)

Building a fan community

Igniting IP-centric content consumption demand

The current global music industry is valued at around $260 billion, with over 2 billion digital music users. This means that the potential market corresponding to the tokenization and financialization of IP far exceeds the traditional crypto user base.

In this context, BeatSwap positions itself at the intersection of "real-world content demand" and "on-chain infrastructure," attempting to bridge the structural gap between content production and financial flow.

BeatSwap's upcoming core product "Space" is scheduled to launch in the second quarter of 2026. This product is defined as the SocialFi layer in the ecosystem, aiming to directly connect creators with users and achieve deep integration with other platform modules.

Key designs include:

A fan-centric interactive mechanism

Exposure and distribution logic based on $BTX staking

User paths connected to DeFi and liquidity structures

Thus, a complete user behavior loop is formed within the platform: Discovery → Participation → Consumption → Rewards → Trading

$BTX is designed to be a core utility asset within the ecosystem, rather than just a simple incentive token, with its value directly tied to platform activity and IP use cases.

Main features include:

· Yield distribution based on on-chain authorized actions

· Value reflection based on IP usage and user engagement dynamics

· Support for staking and DeFi participation mechanisms

· Value growth driven by ecosystem expansion

With the increased frequency of IP use, the utility and value support of $BTX will enhance simultaneously, helping alleviate the "disconnect between value and utility" issue present in traditional Web3 token models to some extent.

Currently, $BTX has been listed on several mainstream exchanges, including:

Binance Alpha

Gate

MEXC

OKX Boost

As the launch of "Space" approaches, BeatSwap is actively pursuing more exchange listings to further enhance liquidity and global accessibility, laying a foundation for future market expansion.

BeatSwap's goal is no longer limited to the traditional Web3 narrative but aims to target over 2 billion digital music users and a trillion KRW-scale content market.

By integrating content creators, users, capital, and liquidity into a blockchain framework centered around IP rights, BeatSwap is striving to build a next-generation infrastructure focused on "IP tokenization."

BeatSwap integrates IP authentication, authorization distribution, incentive mechanism, transaction system, and market construction to establish a unified structure that bridges the full lifecycle path of IP rights.

With the launch of the Q2 2026 "Space," the project is expected to become a key infrastructure connecting content and finance in the IP-RWA (Real World Assets) track.

Mag 7 Evaporates $2 Trillion | Rewire News Morning Edition

Losing $19K per Coin Mined, Bitcoin Mining Firms Collective AI Defection

Morning Report | Tom Lee predicts that the cryptocurrency winter will end in April; xStocks introduces a new on-chain private equity fund; Sui mainnet upgraded to V1.68.1

Polymarket rules have changed, how should airdrop participants respond?

Crypto ETF Weekly | Last week, the net outflow of Bitcoin spot ETFs in the U.S. was $296 million; the net outflow of Ethereum spot ETFs in the U.S. was $206 million

This Week's Key News Preview | The U.S. Releases March Non-Farm Payroll Data; Polymarket Expands Fee Structure

Slow Down, That's the Answer to the Age of the Agent

From Cash to Cryptocurrency: Moving Towards a Unified Regulatory Path for Illegal Payments

Who will own the most Bitcoin in 2026

A private feud lasting 10 years, if not for OpenAI's "hypocrisy," would not have led to the world's strongest AI company, Anthropic

"Crypto Tsar" steps down: 130 days of political performance come to an end, how much of Trump's crypto promise remains?

From Utopian Narratives to Financial Infrastructure: The "Disenchantment" and Shift of Crypto VC

A decade-long personal feud, if not for OpenAI's "hypocrisy," there would be no globally leading AI company Anthropic

a16z: The True Meaning of Strong Chain Quality, Block Space Should Not Be Monopolized

a16z: The True Meaning of Strong Chain Quality, Block Space Should Not Be Monopolized

Cyber Taoist Fortune Teller: Fake Taoist, AI Fortune Telling, and Northeastern Metaphysics History

Bloomberg: Stablecoin Payments Emerge as Crypto VC's Newest Favorite Thing

BeatSwap is evolving towards a full-stack Web3 infrastructure, covering the entire lifecycle of IP rights.

BeatSwap, a global Web3 Intellectual Property (IP) infrastructure project, is attempting to overcome the current fragmentation limitations of the Web3 ecosystem, building a full-stack system that covers the entire lifecycle of IP rights.

Currently, most Web3 projects are still in the stage of functional fragmentation, often focusing only on a single aspect, such as IP asset tokenization, transaction functionality, or a simple incentive model. This structural dispersion has become a key bottleneck hindering the industry's scale application.

BeatSwap's approach is more integrated, integrating multiple core modules into the same system, including:

· IP authentication and on-chain registration

· Authorization-based revenue sharing mechanism

· User-engagement-driven incentive system

· Transaction and liquidity infrastructure

Through the above integration, the platform builds an end-to-end closed-loop path, allowing IP rights to complete a full cycle of "creation, use, and monetization" within the same ecosystem.

BeatSwap is not limited to existing crypto users but is attempting to take the global music industry as a starting point, actively creating new market demand. Its core strategies include:

Exploring and incubating music creators (Artist discovery)

Building a fan community

Igniting IP-centric content consumption demand

The current global music industry is valued at around $260 billion, with over 2 billion digital music users. This means that the potential market corresponding to the tokenization and financialization of IP far exceeds the traditional crypto user base.

In this context, BeatSwap positions itself at the intersection of "real-world content demand" and "on-chain infrastructure," attempting to bridge the structural gap between content production and financial flow.

BeatSwap's upcoming core product "Space" is scheduled to launch in the second quarter of 2026. This product is defined as the SocialFi layer in the ecosystem, aiming to directly connect creators with users and achieve deep integration with other platform modules.

Key designs include:

A fan-centric interactive mechanism

Exposure and distribution logic based on $BTX staking

User paths connected to DeFi and liquidity structures

Thus, a complete user behavior loop is formed within the platform: Discovery → Participation → Consumption → Rewards → Trading

$BTX is designed to be a core utility asset within the ecosystem, rather than just a simple incentive token, with its value directly tied to platform activity and IP use cases.

Main features include:

· Yield distribution based on on-chain authorized actions

· Value reflection based on IP usage and user engagement dynamics

· Support for staking and DeFi participation mechanisms

· Value growth driven by ecosystem expansion

With the increased frequency of IP use, the utility and value support of $BTX will enhance simultaneously, helping alleviate the "disconnect between value and utility" issue present in traditional Web3 token models to some extent.

Currently, $BTX has been listed on several mainstream exchanges, including:

Binance Alpha

Gate

MEXC

OKX Boost

As the launch of "Space" approaches, BeatSwap is actively pursuing more exchange listings to further enhance liquidity and global accessibility, laying a foundation for future market expansion.

BeatSwap's goal is no longer limited to the traditional Web3 narrative but aims to target over 2 billion digital music users and a trillion KRW-scale content market.

By integrating content creators, users, capital, and liquidity into a blockchain framework centered around IP rights, BeatSwap is striving to build a next-generation infrastructure focused on "IP tokenization."

BeatSwap integrates IP authentication, authorization distribution, incentive mechanism, transaction system, and market construction to establish a unified structure that bridges the full lifecycle path of IP rights.

With the launch of the Q2 2026 "Space," the project is expected to become a key infrastructure connecting content and finance in the IP-RWA (Real World Assets) track.